InsureROOFSSM

Confirming Your Roofing Payout

Ai-Screened for Missing Line Items & Incorrect Payout

Proper Indemnification of Your Roofing Payout

If your roof was damaged by a storm or a covered event, the replacement process is fundamentally different from that of a standard retail purchase. Insurance carriers often omit critical line items — drip edge, underlayment layers, flashing, code upgrades — and underpay by using last year's price points. Scan Your Payout Scope to see if it's accurate and up to date.

📄 Upload your Scope of Loss or payout summary — NOT your actual insurance policy.

This is your 1st Payout Offer from your Carrier — the document that tells you what they're willing to pay for your roof.

Not sure which document? Look for “Scope of Loss,” “Estimate,” or “Proof of Loss” from your insurance company — it's the one with line items and dollar amounts.

These are only estimates based on industry best practices. With any insurance claim, your payout should resemble your policy terms and its payment limits. This is not a formal estimate or legal advice. Always consult your policy and a licensed public adjuster or attorney for claim-specific guidance.

Why Insurance Restoration Costs More Than Retail

Retail Roof Purchase

- Pick your material, get a quote, schedule install

- One point of contact (you + contractor)

- Payment at completion

- Standard pricing, straightforward process

Insurance Restoration

- Two adjusters (field + desk) + homeowner + contractor

- Xactimate line-by-line estimating & documentation

- Pre-build, during-build, and post-build photo reports

- Weeks or months waiting on payments (often incorrect)

- Recoverable Depreciation paid only after full documentation is submitted

- Supplement negotiations required for omitted or underscoped line items

Real Scope vs. What's Actually Missing

From an actual Florida carrier estimate (Xactimate). The entire roofing section — vague material, no component breakdown.

CARRIER SCOPE

What the insurance estimate included for roofing

LINE ITEM #3

"Roofing (Bid Item)"

28.00 SQ

No material type. No underlayment. No drip edge. No flashing breakdown at all.

INSUREROOFS℠ FLAGS

What's missing or underscoped — Forgotten by the carrier

- Tear-off not itemized separately

- Underlayment — 2 layers required (FBC 1507.2.8)

- Re-nailing of sheathing (FBC 1521.5) — $???

- Mastic around penetrations (FBC 1507.2.9.3) — $???

- Ice & water shield / valley linings (IRC R905.2.8.2) — $???

- Drip edge — eave & rake (IRC R905.2.8.5) — $???

- Starter strip — $???

- Ridge cap / hip cap — $???

- Step flashing — $???

- Chimney/counter flashing (IRC R903.2.1) — $???

- Pipe boot / jack flashing — $???

- Ridge vent / ventilation — $???

- Decking repair (plywood/OSB) — $???

- Permits & engineering — $???

- O&P (10%+10%) — $0

New Total:

$??? + $??? + $???

= Much More Than $7,810

*All results will vary. No guarantees of increase.

14+ items missing or unspecified

Source: Based on actual Florida carrier estimate patterns (Xactimate). Homeowner info removed. Roofing area data only.

InsureROOFS℠ Scope Scanner — $49.95

Our InsureROOFS℠ Ai-powered Scope Scanner will analyze your carrier's document, identify roofing line items, flag missing charges, and compare their pricing against actual North Florida contractor rates.

✅ FREE Scan

Available if you A) live in our local service area (Duval / St Johns / Clay / Nassau County) AND B) are willing to sign a Contingency Agreement with P1Mitigators™ — allowing us to help get you paid for the roofing and then hiring us to handle the install (or pay a cancellation fee of 25%).

💰 Paid Scan — $49.95

For out-of-area homeowners or anyone who prefers the full report without a contingency agreement. Pay $49.95, upload your scope, and get the complete InsureROOFS℠ analysis delivered to your email.

Pay $49.95 via Stripe →InsureROOFS℠ is a Service Marked(SM) Process Created, Owned, Protected and Copyrighted by Proxy1MEDIA LLC.

Xactimate Full Reporting — $499.95

Get this month's Xactimate price points — the same system insurance carriers use to calculate your payout. Know exactly what your claim should include before your contractor submits.

What's Included — $499.95 Pre-Paid

- Xactimate pricing for your roof replacement

- Xactimate pricing for your fence replacement

- Xactimate pricing for two interior rooms

- Current-month price points (not last year's data)

What You Need to Provide

- • Minimum 10 photos covering all 4 areas:

- — Roof (from ground level, all sides + any visible damage)

- — Fence (all damaged sections + gates)

- — Interior Room #1 (walls, ceiling, floor)

- — Interior Room #2 (walls, ceiling, floor)

- • Square footage listing of your home

These are only estimates based on industry best practices. This is not a formal estimate or legal advice.

Our Insurance Restoration Process

Upload Your Scope of Loss

Upload the roofing portion of your insurance estimate. Our AI scans it instantly for missing line items and underpaid charges.

We Review & Compare

Our team compares your carrier's scope against actual North Florida contractor pricing and current Xactimate price points, line by line.

Supplement If Needed

If items are missing or underpaid, we help you prepare a supplement with proper documentation, code references, and Xactimate-supported pricing.

Build & Document

We install your roof with full pre-build, during-build, and post-build photo documentation required for RD recovery.

Help You Recover RD

After completion, we provide all documentation needed for your carrier to release the Recoverable Depreciation payment.

Insurance Claim?

Let InsureROOFSSM Help.

We work with all major carriers. Free scope reviews for local homeowners — start by uploading your scope or exploring our tools.

These are only estimates based on industry best practices. With any insurance claim, your payout should resemble your policy terms and its payment limits. This is not a formal estimate or legal advice. Always consult your policy and a licensed public adjuster or attorney for claim-specific guidance.

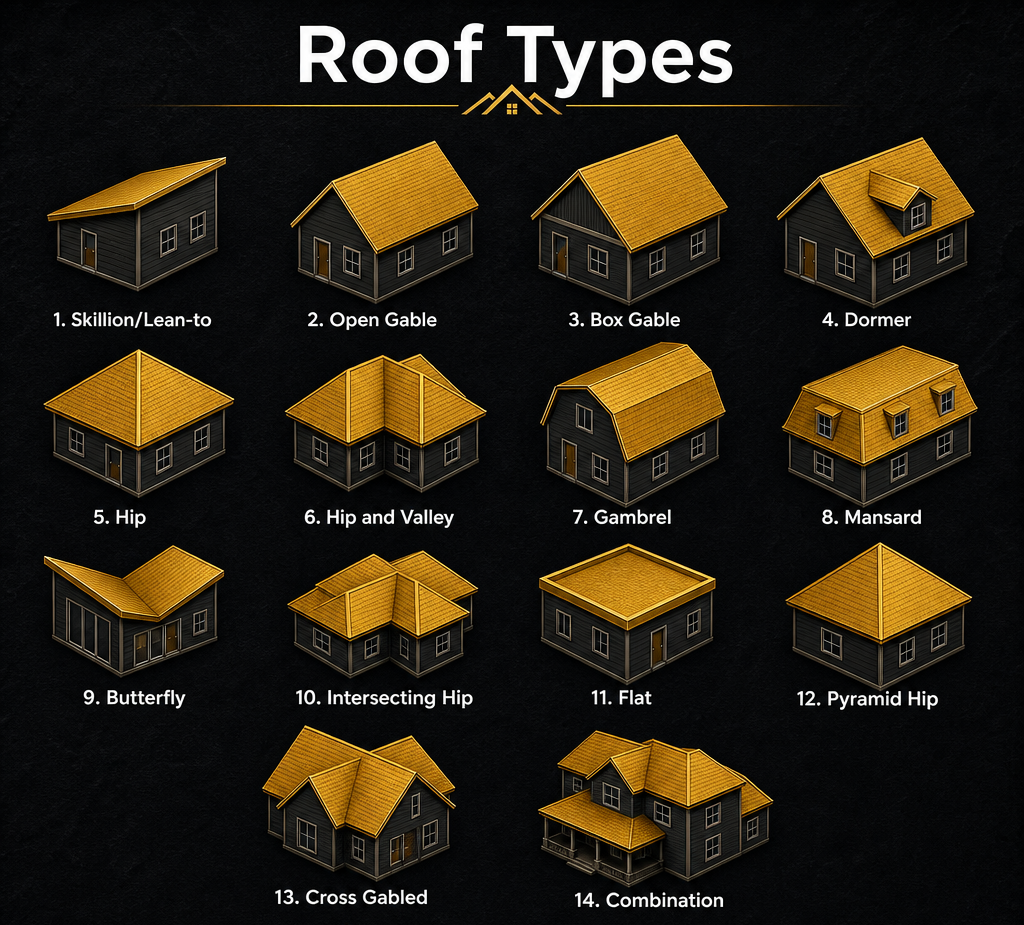

Roof Types Reference